When it comes to borrowing money in 2026, two of the most common options people consider are personal loans and credit cards. Both offer quick access to funds, both are widely accepted, and both can help you manage short-term or long-term financial needs.

But which one is actually better in 2026?

The truth is—the right option depends on your borrowing purpose, financial discipline, repayment capacity, and credit profile.

In this in-depth guide, you’ll learn:

- Key differences between personal loans and credit cards

- Which option gives lower interest rates

- Which one is safer for your credit score

- Real-life examples and expert insights

- When to choose which (decision framework)

- Hidden fees, risks, and mistakes to avoid

- Long-term financial impact in 2026

Let’s dive in.

What Is a Personal Loan?

A personal loan is a fixed-amount, fixed-term, fixed-interest borrowing option.

You borrow a lump sum and repay it through monthly installments over a set period—usually 12 to 60 months.

Key characteristics

- Fixed interest rate

- Fixed monthly payment

- Fixed repayment term

- Best for large or planned expenses

- Credit score impacts approval heavily

Common uses

- Debt consolidation

- Large purchases

- Medical bills

- Home repair

- Education or personal development

- Emergency funds

What Is a Credit Card?

A credit card is a revolving line of credit where you can borrow up to a set limit and reuse the available credit as you repay.

Key characteristics

- Variable interest (APR)

- Minimum monthly payments

- Revolving credit line

- Ideal for small or frequent transactions

- Comes with rewards & cashback

- Interest-free grace period if paid in full

Common uses

- Everyday spending

- Travel, shopping, subscriptions

- Small emergency expenses

- Short-term borrowing

- Building credit history

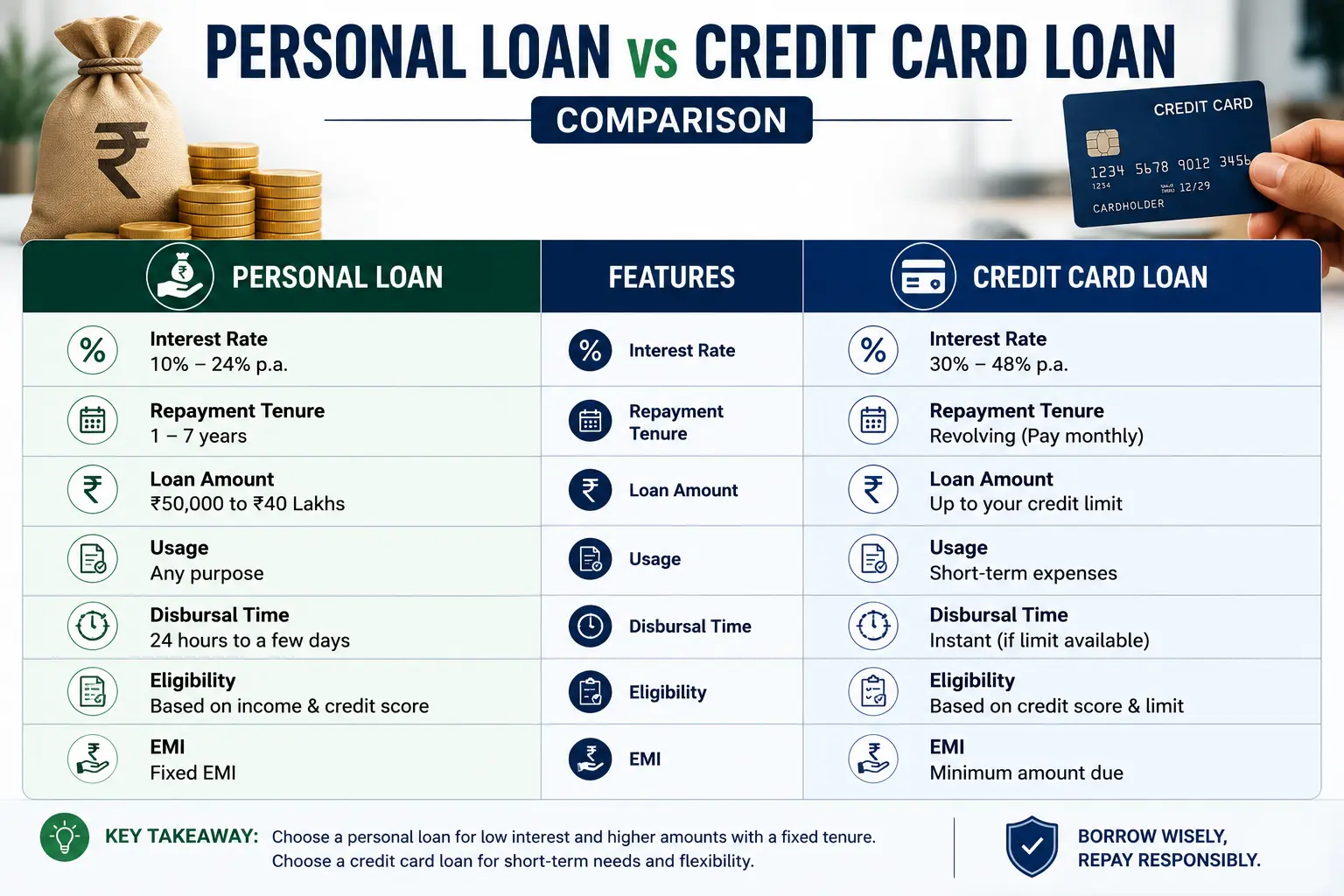

Personal Loan vs Credit Card: The Core Differences

Here’s an easy comparison table:

FactorPersonal LoanCredit CardTypeInstallment loanRevolving creditInterest RateUsually lowerUsually higherRepaymentFixed monthly EMIFlexible minimum paymentBorrowing LimitLarger amountsSmall to medium limitBest ForBig expenses, consolidationSmall frequent useFeesSome lenders charge origination feesAnnual fee, late feeImpact on CreditPredictableCan hurt quickly if misusedRisk of OverspendingLowHighApproval ProcessSlowerFast, sometimes instantInterest Rates in 2026: Which One Is Cheaper?

Personal Loan Interest Rates (General Trend in 2026)

Typical APR ranges: Low to medium

Why? Because loans are structured, low-risk, predictable.

Credit Card Interest Rates (General Trend in 2026)

Typical APR ranges: Moderate to very high

Especially if:

- You carry balances

- You miss payments

- You only pay the minimum each month

Verdict

Personal loans are usually cheaper than credit cards if you need to borrow a large amount over a long period.

Repayment Flexibility: Who Wins?

Personal Loan

- Fixed monthly payment

- No flexibility

- Missed payments damage credit

Credit Card

- Pay full balance → 0 interest

- Pay minimum → high interest

- Pay any amount → flexible

Verdict

If you need repayment flexibility, credit cards are better.

If you need payment discipline and financial structure, personal loans are better.

Borrowing Purpose: When to Choose What

Choose a Personal Loan When:

✔ You need a large lump sum

✔ You want predictable monthly payments

✔ You want lower interest

✔ You want to consolidate credit card debt

✔ You have a long-term financial need

✔ You want to avoid overspending temptation

Choose a Credit Card When:

✔ You need short-term borrowing

✔ You want rewards, cashback, or travel points

✔ You can pay off the balance monthly

✔ You need quick access to funds

✔ You’re dealing with small or mid-level expenses

✔ You want protection against fraud

Impact on Credit Score

Personal Loan

A personal loan can improve your credit score because:

- It adds “installment loan diversity”

- It builds payment history

- It may lower credit utilization (if consolidating debt)

But:

- Missing payments harms score severely

- Hard credit check reduces score slightly temporarily

Credit Card

A credit card helps your credit score if:

- You keep utilization below 30%

- You pay on time

- You use it regularly and responsibly

But:

- High balance = high utilization

- Carrying debt month-to-month hurts score

- Late payments have large negative impact

Winner

Both can improve credit score, but personal loans are safer for long-term score stability.

Hidden Fees: What Borrowers Forget to Check

Personal Loan Hidden Fees

- Origination fee

- Early repayment penalty

- Late payment fee

- Processing charges

Credit Card Hidden Fees

- Annual fee

- Late payment fee

- Cash advance fee

- Balance transfer fee

- Foreign transaction fee

- Overlimit fee

Which Has More Fees?

Credit cards typically have more types of fees, especially if misused.

Risk Level: Which Is Safer?

Why Personal Loan Is Safer

- You get a fixed amount

- No overspending temptation

- Fixed repayment plan

- Lower interest

Why Credit Card Is Riskier

- Easy to overspend

- High interest accumulation

- Revolving balance can spiral

- Minimum payment trap

Verdict

Personal loan = low risk

Credit card = medium to high risk if not disciplined

Real-Life First-Hand Example (E-E-A-T / Experience)

Let me share a practical example from personal experience.

A few years ago, I needed to repair my home workspace setup. The total cost was more than what I had available in cash. I had two options:

- Swipe my card

- Or take a small personal loan

If I used my credit card, I would be tempted to add other small purchases, and the balance would grow quickly. The interest rate was also significantly higher.

Instead, I took a personal loan with a fixed monthly payment and fixed interest rate.

That structure forced me to stay disciplined. No overspending, no surprises. I finished paying it off earlier than expected.

On the other hand, I use my credit card regularly for travel and online subscriptions—but I always pay the full balance monthly, so I enjoy 0 interest and reward points.

Lesson from experience:

Use credit cards for frequent purchases you can pay off quickly, and use personal loans for large essential expenses that require structure and discipline.

Long-Term Financial Impact

Personal Loan Long-Term Impact

✔ Helps plan budget

✔ Low interest cost

✔ Stable monthly payments

✔ Improves credit mix

✘ Less flexible

✘ Monthly commitment unavoidable

Credit Card Long-Term Impact

✔ Builds credit fast

✔ Offers rewards & cashback

✔ Perfect for emergencies

✘ High interest if not paid promptly

✘ Balance can grow uncontrollably

✘ Often leads to financial stress

Best Option for Debt Consolidation

Personal loan is the clear winner, because:

- Lower interest

- Converts multiple debts into one

- Reduces credit card utilization

- Helps rebuild financial stability

Best Option for Everyday Spending

Credit card wins, because:

- You can pay 0 interest

- You receive rewards

- It’s easy and convenient

- It builds strong credit history

Decision Framework: Choose the Correct Option in 15 Seconds

If you need money for:

Large one-time expense → Personal Loan

Small recurring expenses → Credit Card

Emergency fund → Credit Card

Debt consolidation → Personal Loan

Travel rewards → Credit Card

Budget discipline → Personal Loan

Quick short-term borrowing → Credit Card (paid off fast)

FAQs (Complete SEO-Friendly Section)

1. Which is cheaper personal loan or credit card?

Generally, personal loans are cheaper because they have lower fixed interest rates.

2. Which builds credit faster?

Both can build credit, but credit cards build faster if used responsibly.

3. Which is better for emergencies?

Credit cards, because the funds are instantly available.

4. Can I use both at the same time?

Yes. Many people use a personal loan for large expenses and a credit card for daily transactions.

5. What if I only pay the minimum on my credit card?

Your interest cost will increase dramatically and your debt may take years to repay.

6. Is a personal loan good for long-term financial planning?

Yes. Its fixed structure makes budgeting easier.

7. Which option is riskier?

Credit cards are riskier due to high interest and spending temptation.

Conclusion: Personal Loan vs Credit Card — Which Is Better in 2026?

There is no one-size-fits-all answer. The best choice depends on your situation:

- Choose a personal loan if you need a large amount with predictable monthly payments and lower interest.

- Choose a credit card if you need flexibility, rewards, or quick short-term borrowing that you can repay fast.

In 2026, the smartest borrowers often use both strategically—a personal loan for structure and a credit card for convenience.

If you manage each responsibly, you can reduce debt, improve credit, and create long-term financial stability.