Introduction

When people talk about their annual income, they often mention the total salary they earn before taxes. However, that number doesn't accurately reflect how much money is actually available to spend throughout the year. The amount that truly matters for everyday life is annual income after taxes, which represents the money left after required taxes have been deducted from your earnings. Whether you're creating a budget, comparing job offers, planning your savings, or preparing for retirement, understanding this figure helps you make more informed financial decisions.

Many people make the mistake of planning their expenses around their gross salary. While the gross amount may look impressive, it doesn't account for taxes that reduce your take-home pay. This can lead to unrealistic budgets, overspending, and difficulty reaching financial goals. Learning how annual income after taxes works gives you a clearer picture of your real financial situation and allows you to make smarter decisions with your money.

In this guide, you'll learn what annual income after taxes means, how it's calculated, why it's important, and how it can affect your personal finances. You'll also discover practical examples and useful tips that make this financial concept easy to understand.

What Does Annual Income After Taxes Mean?

Annual income after taxes is the total amount of money you keep over an entire year after all required taxes have been deducted from your gross income. It is often called net annual income, after-tax income, or take-home income, and it represents the money that is actually available for your daily expenses, savings, investments, and financial goals.

Unlike gross income, which shows your earnings before any deductions, annual income after taxes reflects your real purchasing power. This is the amount that reaches your bank account and can be used to pay rent or a mortgage, buy groceries, cover utility bills, build an emergency fund, or invest for the future. Because it represents the income you can actually use, it is considered one of the most important financial figures for individuals and families.

For employees, taxes are usually withheld automatically from each paycheck by the employer. By the end of the year, the total amount remaining after those tax deductions becomes your annual income after taxes. If you are self-employed, you generally calculate this amount after determining your yearly tax obligations and subtracting them from your gross earnings.

Gross Income vs. Annual Income After Taxes

Gross income and annual income after taxes are closely related, but they represent two very different financial concepts. Gross income is the total amount you earn before any taxes or mandatory deductions are taken out. It is the figure commonly listed in employment contracts, job advertisements, and salary negotiations because it reflects your complete earnings before taxes are applied.

Annual income after taxes, on the other hand, is the amount you actually receive after taxes have been deducted. This is your real take-home income and the amount you have available to cover living expenses, save for future goals, and invest. Since taxes reduce your overall earnings, your after-tax income will always be lower than your gross income.

For example, imagine someone earns a gross annual salary of $80,000. If they pay $16,000 in taxes during the year, their annual income after taxes would be $64,000. While the gross salary may appear to be the larger and more attractive number, the after-tax income is the amount that truly determines their financial flexibility.

When comparing job opportunities or creating a personal budget, relying only on gross income can be misleading. Two jobs with similar salaries may result in different take-home pay depending on tax deductions and other financial factors. This is why financial professionals recommend using annual income after taxes when evaluating your overall financial position.

Why Annual Income After Taxes Matters

Understanding your annual income after taxes is essential because it provides the most accurate picture of your financial health. It helps you understand exactly how much money you have available after meeting your tax obligations, making it easier to plan for both short-term and long-term financial goals.

When creating a monthly budget, your after-tax income should always be your starting point. Since this is the money that actually reaches your account, it allows you to estimate your spending limits more accurately and avoid budgeting mistakes based on income you never receive. It also helps you decide how much you can comfortably save each month, invest for retirement, or use to pay off debt.

Annual income after taxes is also valuable when comparing employment opportunities. A higher salary doesn't always translate into significantly higher take-home pay because taxes can reduce the difference between two job offers. Looking at your estimated after-tax income gives you a more realistic basis for comparing compensation packages.

From personal experience, one of the simplest ways to improve financial planning is to ignore your gross salary when building a budget. Instead, focus only on the amount that actually appears in your bank account after taxes. This small change makes it much easier to control spending, stay within your budget, and consistently work toward your financial goals.

How Annual Income After Taxes Is Calculated

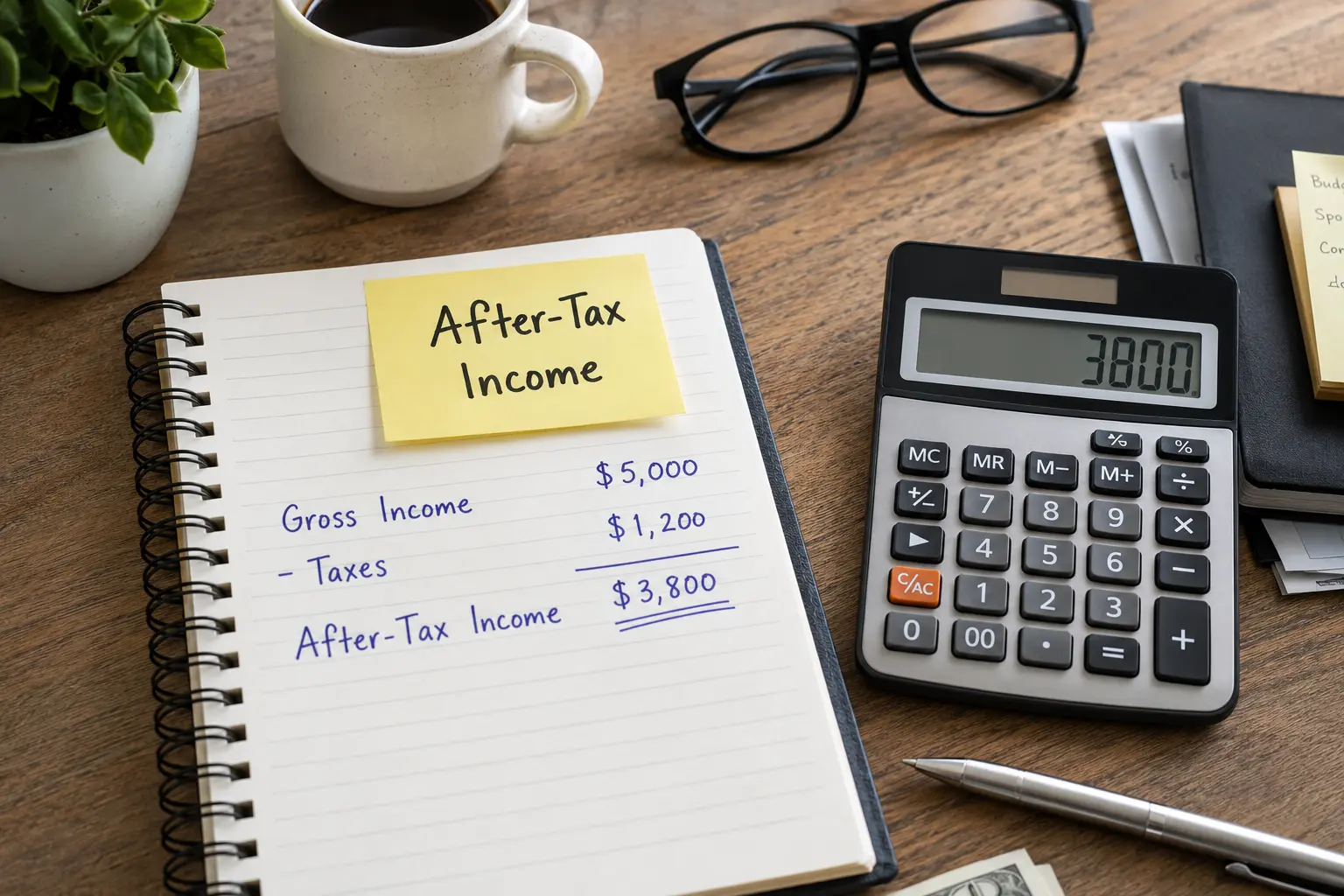

Calculating annual income after taxes is relatively straightforward. You begin with your gross annual income, which is the total amount you earn before taxes, and subtract the total taxes you pay throughout the year. The remaining amount is your annual income after taxes, also known as your net annual income.

The basic formula is:

Annual Income After Taxes = Gross Annual Income − Total Taxes Paid

The taxes deducted may include income taxes, payroll taxes, and other mandatory tax obligations, depending on your circumstances. It's important to remember that voluntary deductions, such as retirement contributions or insurance premiums, may be treated differently depending on the financial calculation being used.

For example, if your gross annual income is $75,000 and you pay $15,500 in total taxes during the year, your annual income after taxes would be $59,500. This is the amount you would use when planning your budget, setting savings goals, or evaluating your overall financial position.

Although the calculation itself is simple, your final after-tax income can vary based on several factors, including your tax situation, available tax credits, and the amount of taxable income you earn. Understanding this calculation helps you estimate your take-home pay more accurately and make better financial decisions throughout the year.

Monthly After-Tax Income

While annual income after taxes gives you a yearly overview of your finances, converting it into a monthly figure makes it much easier to manage everyday expenses. Most people pay their rent or mortgage, utilities, groceries, insurance, and other bills every month, so knowing your monthly take-home income provides a more practical foundation for budgeting. You can calculate it by dividing your annual after-tax income by twelve. For example, if your annual income after taxes is $72,000, your monthly take-home income would be approximately $6,000. Using this amount instead of your gross monthly salary helps you create a budget that reflects your actual financial situation and reduces the risk of overspending.

Weekly After-Tax Income

Some employees receive their wages every week, making weekly after-tax income an important figure for managing short-term expenses. To estimate your weekly take-home pay, simply divide your annual after-tax income by 52 weeks. This calculation helps you understand how much money is available each week for groceries, transportation, entertainment, and other recurring costs. Tracking your finances on a weekly basis can also make it easier to identify unnecessary spending before it affects your monthly budget.

Biweekly After-Tax Income

Many employers pay their employees every two weeks instead of weekly or monthly. In this case, your annual after-tax income can be divided by 26 pay periods to estimate your biweekly paycheck. Knowing this amount is especially useful when planning large expenses or setting aside money for savings each payday. Since two months each year contain three biweekly paychecks, many people use those extra pay periods as an opportunity to boost savings or pay down debt more quickly.

Why Two People With the Same Salary Can Have Different After-Tax Income

It is common to assume that two people earning the same annual salary will receive identical take-home pay, but this is rarely the case. Taxes vary depending on several personal financial factors, including filing status, available tax credits, retirement contributions, and additional taxable income. Some individuals may also have different payroll deductions or withholding elections that affect the amount deducted from each paycheck. As a result, even employees with identical gross salaries can end up with noticeably different annual income after taxes. This is why comparing only salaries doesn't always provide a complete picture of someone's financial situation.

Common Sources of Annual Income

Annual income is not limited to a regular salary. Many people earn money from multiple sources throughout the year, and each source may affect their overall tax liability. Common examples include wages, overtime pay, bonuses, commissions, freelance work, business profits, rental income, investment earnings, pensions, and self-employment income. Since many of these earnings are taxable, they contribute to your total annual income and ultimately influence how much money remains after taxes have been paid.

What Is Included in Annual Income After Taxes?

Annual income after taxes generally includes all taxable earnings that remain after required taxes have been deducted. This typically covers wages, salaries, overtime pay, bonuses, commissions, and other forms of taxable compensation. The final amount represents the money you actually receive and can use for daily living expenses, saving, or investing. Although the exact definition may vary depending on the financial institution or report, after-tax income usually reflects your actual take-home earnings rather than your total salary before deductions.

What Is Not Included?

Annual income after taxes does not include the taxes you paid during the year because those amounts have already been deducted from your earnings. It also excludes your gross income before taxes, as that figure does not represent money available for spending. Depending on the financial context, certain voluntary deductions, such as retirement contributions or insurance premiums, may also be excluded when calculating your final take-home income. Understanding what is and is not included helps prevent confusion when reviewing pay stubs, tax documents, or financial statements.

Why Employers Mention Gross Salary Instead of After-Tax Income

Employers almost always advertise jobs using gross annual salary rather than after-tax income because taxes are different for every employee. Factors such as tax status, deductions, credits, and additional sources of income all affect the amount of tax someone ultimately pays. Since employers cannot accurately predict an individual's tax situation, they present compensation using gross earnings. It's the employee's responsibility to estimate how much of that salary will remain after taxes to determine their expected take-home pay.

Annual Income After Taxes for Budgeting

Creating a budget based on your annual income after taxes is one of the most effective ways to manage your finances. Because this figure represents the money you actually receive, it provides a realistic foundation for planning monthly expenses, building an emergency fund, paying off debt, and investing for the future. Many budgeting mistakes happen because people focus on their gross salary instead of their take-home income. By using your after-tax earnings as the starting point, you can avoid spending money that never reaches your bank account and make more confident financial decisions.

How Annual Income After Taxes Affects Loan Applications

Your annual income after taxes can also play an important role when applying for loans or other forms of financing. While lenders often review your gross income during the approval process, your take-home income gives a clearer picture of how much money you actually have available to make monthly payments. A healthy after-tax income can improve your ability to manage loan repayments without placing unnecessary strain on your budget. Understanding your real disposable income before borrowing can also help you avoid taking on more debt than you can comfortably afford.

Annual Income After Taxes and Retirement Planning

Planning for retirement becomes much easier when you understand your annual income after taxes. Since your take-home pay represents the money available after meeting your tax obligations, it determines how much you can realistically contribute toward long-term savings each year. Rather than basing retirement goals on your gross salary, using your after-tax income creates a more practical savings strategy that fits your everyday financial needs. Even small, consistent contributions based on your take-home income can grow significantly over time and help build greater financial security for the future.

Annual Income After Taxes and Saving Money

Your annual income after taxes plays a major role in determining how much money you can realistically save each year. Since this is the amount that actually reaches your bank account, it provides the most accurate starting point for setting savings goals. Whether you're building an emergency fund, saving for a home, planning a vacation, or investing for the future, your after-tax income should guide your decisions. Financial experts often recommend saving a percentage of your take-home pay rather than your gross salary because it reflects the money you truly have available. By consistently saving from your after-tax income, you can create a sustainable financial plan that supports both short-term needs and long-term goals.

Common Mistakes People Make

Many people misunderstand annual income after taxes, which can lead to poor financial decisions. One of the most common mistakes is creating a budget based on gross income instead of take-home pay. Since taxes reduce the amount you actually receive, relying on gross earnings often results in overspending and financial stress. Another common mistake is forgetting that bonuses, commissions, or overtime pay may be taxed differently, meaning the amount deposited into your account may be lower than expected. Some people also ignore changes in tax withholding or fail to review their pay stubs regularly, making it difficult to understand where their money is going. Avoiding these mistakes can help you maintain better control over your finances throughout the year.

Personal Experience and Practical Tip

One budgeting habit that has consistently proven effective is focusing only on take-home income instead of gross salary. Early in my financial planning, I realized that using the salary listed on a job offer created unrealistic expectations because taxes reduced the actual amount available each month. Once I started building my budget around the money that actually arrived in my bank account, managing expenses became much easier. Saving money felt more achievable, unexpected bills became less stressful, and I no longer relied on income that I never truly received. If you're starting a new job or reviewing your finances, compare your estimated after-tax income with your first few paychecks. This simple habit can help you make small adjustments early and avoid budgeting problems later.

what is annual income mean

How Increase Your Annual Income After Taxes

Although paying taxes is a normal part of earning income, there are several legitimate ways to improve the amount of money you keep after taxes. Reviewing your tax withholding regularly can help prevent paying too much throughout the year and may improve your cash flow. Taking advantage of available tax credits and deductions can also reduce your overall tax bill if you qualify. Contributing to eligible retirement accounts may lower your taxable income while helping you build long-term wealth. If you earn income from freelance work or a business, keeping organized records of deductible expenses can also reduce your taxable income. Finally, reviewing your financial situation each year and seeking professional tax advice when necessary can help you identify opportunities to legally maximize your after-tax income.

Conclusion

Understanding what annual income after taxes means is essential for making informed financial decisions and building long-term financial stability. While gross income may be the number most commonly discussed, your after-tax income is the amount that truly reflects your purchasing power and determines how much money you have available to spend, save, and invest. By focusing on your take-home income instead of your gross salary, you can create a more realistic budget, compare job opportunities more accurately, prepare for major financial goals, and avoid common budgeting mistakes. Whether you're starting your career, changing jobs, or improving your overall financial health, using your annual income after taxes as the foundation of your financial planning will help you make smarter decisions and achieve greater confidence in managing your money.

Frequently Asked Questions

Is annual income after taxes the same as net income?

Yes. In most personal finance situations, annual income after taxes and net income refer to the same thing. Both describe the amount of money you keep after all required taxes have been deducted from your gross annual earnings.

Why is my annual income after taxes lower than my salary?

Your salary usually represents your gross income before taxes are deducted. Income taxes and other mandatory payroll taxes reduce the amount you actually receive, resulting in a lower annual income after taxes.

How can I calculate my annual income after taxes?

You can calculate your annual income after taxes by subtracting the total taxes paid during the year from your gross annual income. The remaining amount is your net or after-tax income.

Should I budget using gross income or after-tax income?

You should always budget using your after-tax income because it reflects the money that is actually available for spending, saving, and investing. This approach creates a more realistic and sustainable financial plan.

Can annual income after taxes change every year?

Yes. Your after-tax income may change due to salary increases, bonuses, changes in tax laws, different tax withholding amounts, or additional sources of taxable income. Reviewing it annually helps keep your financial plans accurate.

Does annual income after taxes include bonuses?

Yes. If your bonus is taxable, the amount you receive after taxes becomes part of your annual income after taxes. However, bonuses may be taxed differently from regular wages depending on your tax situation.

Why do online after-tax income calculators give different results?

Different calculators use different assumptions about tax rates, deductions, retirement contributions, and filing status. Because everyone's financial situation is unique, the estimated after-tax income may vary slightly between calculators.